Spain Property Interest Rate Forecast 2026: Towards a Decline in Euribor?

Introduction

Are you planning a property purchase in Spain and asking the most crucial financial question: what will be the Spanish property interest rate forecasts in 2026? After the volatility and rapid increases of 2023 and 2024, it's natural to seek clarity. As experts in the Spanish real estate market, we must be clear: no one can predict the exact figure. Financing involves significant financial decisions, and a "forecast" should be an analysis of factors, not a crystal ball.

The key to understanding Spanish interest rates is not in Madrid, but in Frankfurt, at the headquarters of the European Central Bank (ECB). Mortgage rates in Spain (fixed or variable) are directly linked to the Euribor index, which itself follows the ECB's decisions on inflation. This article analyzes the probable scenarios for 2026 and their concrete impact on your borrowing capacity as a non-resident buyer.

Euribor: The True Driver of Spanish Rates

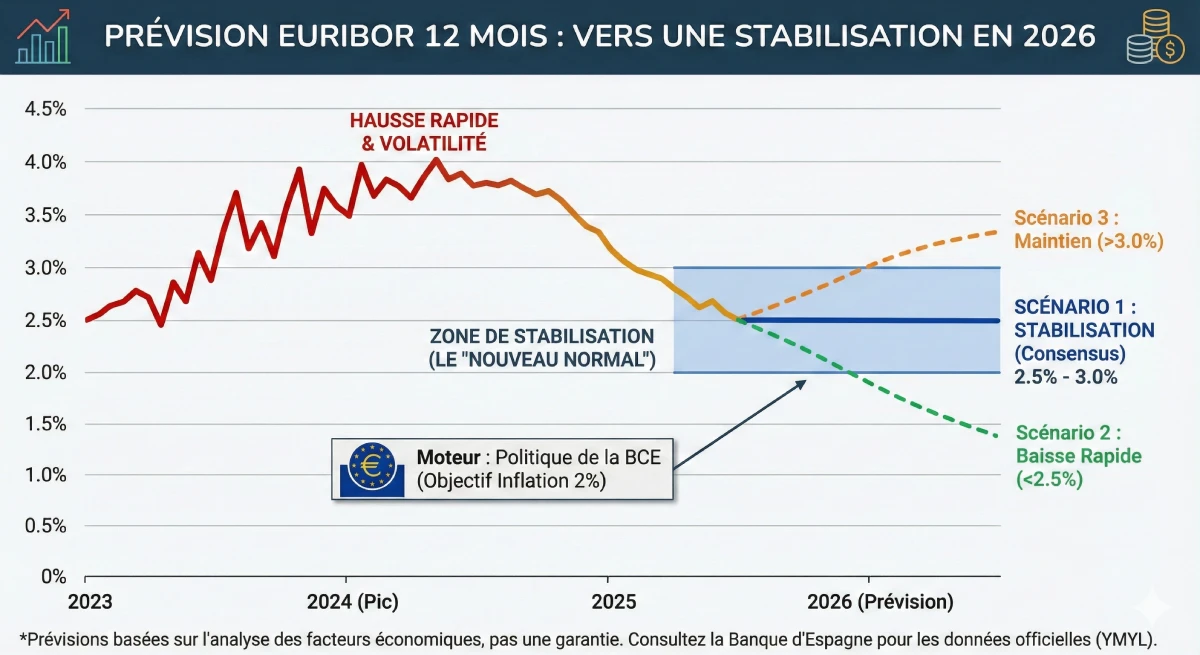

Forget everything else: if you want to know the future of Spanish interest rates, you must monitor the 12-month Euribor. This is the benchmark index upon which almost all Spanish banks (Santander, CaixaBank, BBVA, Sabadell...) base their loan offers, especially variable rates.

Euribor represents the rate at which European banks lend money to each other. It is directly correlated with the ECB's key interest rate. The ECB's objective is to maintain inflation in the Eurozone at 2%. The rate hikes of 2023-2024 aimed to curb inflation. Future rate cuts will only occur when the ECB is convinced that this 2% target is sustainably achieved.

Euribor Forecasts and Scenarios for 2026

After the 2024 peak, the consensus among analysts (such as those at Bankinter and other financial institutions) points towards normalization and stabilization. The era of 0% interest rates is over. We are entering a "new normal" where rates will settle at a healthier level for the economy.

Here are the three most probable scenarios for the 12-month Euribor in 2026:

- ✅ Scenario 1 (Realistic/Consensus): Stabilization. Inflation is controlled around 2%. The ECB has implemented its rate cuts in 2025. Euribor stabilizes within a healthy range, between 2.5% and 3.0%. Spanish banks offer fixed rates around 3.0% - 3.5%.

- 📉 Scenario 2 (Optimistic): Rapid Decrease. The Eurozone economy slows more than expected. The ECB must cut rates quickly to stimulate growth. Euribor could temporarily fall below 2.5%.

- 📈 Scenario 3 (Pessimistic): Sustained High Rates. Inflation proves persistent ("sticky"). The ECB is forced to keep its key interest rates high for longer. Euribor would then remain above 3.0%, possibly even 3.5%.

Fixed vs. Variable Rates in 2026: The New Choice

In Spain, the choice between a `tipo fijo` (fixed rate) and a `tipo variable` (variable rate) is a real dilemma. A variable rate is calculated as follows: 12M Euribor + Bank Margin (the `diferencial`). If Euribor is at 2.5% and your margin is +0.7%, your rate is 3.2% (revisable annually).

| Rate Type | Main Advantage | Main Risk | Who is it for in 2026? |

|---|---|---|---|

| Fixed Rate (`Fijo`) | Absolute security. Your monthly payment is locked in for the life of the loan, regardless of ECB decisions. | You pay an "insurance premium". If Euribor plummets, you won't benefit. | The cautious non-resident buyer who wants complete visibility on their budget. |

| Variable Rate (`Variable`) | If Scenario 2 (decrease) materializes, your monthly payment will decrease over the years. | Uncertainty. If Scenario 3 (sustained high rates) occurs, your monthly payments will remain high. | The investor or buyer who firmly believes in a sustainable drop in Euribor below 2.5%. |

Expert Advice: The Mixed Rate Loan (`Tipo Mixto`)

The most popular product in Spain right now is the mixed rate loan. The bank offers you a fixed rate for the first 5, 7, or 10 years, then the loan switches to a variable rate (Euribor + margin). It's a good compromise to have security at the start, while betting on a long-term decline in Euribor.

Impact: Your Borrowing Capacity in 2026

An interest rate forecast is only useful if applied to your specific project. The interest rate has a direct impact on your borrowing capacity. Remember that as a non-resident, a Spanish bank will only finance 60% to 70% of the purchase price.

Let's look at the impact of a "stabilized" rate (Scenario 1) on the same monthly payment, compared to the era of zero rates.

| Characteristic | Scenario A (Rate at 1.0%) | Scenario B (Rate at 3.0%) |

|---|---|---|

| Target Monthly Payment | ~€800 | ~€800 |

| Loan Term | 20 years | 20 years |

| Borrowing Capacity (max) | ~ €175,000 | ~ €145,000 |

| Impact | With the same monthly payment, you can borrow €30,000 less with a 3.0% rate than with a 1.0% rate. | |

Official Resource & Disclaimer

All forecasts are, by definition, uncertain. The only fact is the current rate. For official data on interest rates and Euribor, the sole authoritative source is the Bank of Spain (Banco de España).

This article does not constitute financial advice. Consult the official statistics of the Bank of Spain and speak to a qualified financial advisor.

Conclusion

In conclusion, Spanish property interest rate forecasts for 2026 point towards stabilization. The era of 0% rates is over. The most probable scenario is Euribor maintaining within a range of 2.5% to 3.0%, allowing banks to offer fixed rates around 3.0% to 3.5%.

For a non-resident buyer, this means that borrowing capacity remains lower than a few years ago. The key to your project in 2026 will be to have a **strong personal down payment** (at least 40-50% of the total price, including fees) and to aggressively compare bank offers, looking beyond the advertised rate (pay attention to insurance and related products, known as `bonificaciones`).

Your Borrowing Capacity in 2026?

Take advantage of market opportunities. Let's discuss your project.

FAQ: Spanish Mortgage Rate Predictions 2026

Addressing Your Key Questions on Euribor, the ECB, and How Evolving Rates Impact Your Borrowing Capacity in Spain for 2026.

YMYL (Your Money Your Life) & E-E-A-T Advisory

These forecasts and analyses are based on our established expertise (E-E-A-T) and current market consensus. Property financing is a YMYL (Your Money Your Life) topic, carrying inherent risks and depending entirely on your personal circumstances. This article does not constitute financial advice. We strongly recommend consulting a qualified financial advisor or mortgage broker for a personalised analysis.

The most probable scenario (analyst consensus) is stabilisation. The era of 0% rates is over. The 12-month Euribor index, which dictates Spanish rates, is expected to stabilise within a healthy range of 2.5% to 3.0%. Fixed rates offered by banks should be just above this, between 3.0% and 3.5%.

The ECB sets key interest rates for the entire Eurozone to control inflation (targeting 2%). The Euribor (the rate at which banks lend money to each other) closely follows these decisions. As Spanish banks use Euribor as the calculation basis for their loans (especially variable ones), any decision by the ECB in Frankfurt has a direct impact on your monthly mortgage payment in Alicante or Marbella.

Euribor (Euro Interbank Offered Rate) is the "cost of money" for banks. If the bank lends to you at a variable rate, it will charge you: [12M Euribor Rate] + [Its fixed commercial margin]. For example, if Euribor is 2.7% and the bank's margin is 0.8%, your interest rate will be 3.5%. This rate is revised annually based on the new Euribor.

A fixed rate is an "insurance" you pay to the bank. The bank bets that the average Euribor will be below 3.3% over the term of your loan. You therefore pay a premium (the 0.5% difference) for the security and peace of mind of knowing that your monthly payment will never change, even if Euribor rises to 4% or 5%.

There is no "best" choice; it all depends on your risk profile (YMYL):

- ✅ Fixed: For cautious buyers (especially non-residents) who want total budget security.

- ✅ Variable: For investors who anticipate a fall in rates below 2.5% and can afford a rise in monthly payments if their bet fails.

- ✅ Hybrid: The right compromise. You benefit from a secure fixed rate for 5 or 10 years, then switch to a variable rate, betting that Euribor will be low at that time.

It's a risk/reward calculation. If you wait, rates might be slightly lower (for example, Euribor at 2.7% instead of 3.0%). However, if buyer demand picks up due to this drop, property prices could increase, negating any gain from the lower rate. Many experts consider rate stabilisation a good time to buy, as it offers clarity.

Yes, it is the most critical impact. As the article shows, for the same monthly payment of €800 over 20 years, a rate of 3.0% allows you to borrow €30,000 less than a rate of 1.0%. Your borrowing capacity is directly reduced by rising rates.

Yes. Euribor is the same for everyone. The difference for a non-resident is not the base rate, but:

- The bank's margin (diferencial), which may be slightly higher.

- The loan-to-value (LTV), which is capped at 60-70% (compared to 80% for a resident).

No. A pre-approval ("pre-aprobación") is simply a non-binding solvency study. The firm and definitive loan offer, the FEIN (Ficha Europea de Información Normalizada - European Standardised Information Sheet), is only issued once you have a specific property (with an appraisal/valuation). This offer has a very short validity period (a few weeks), so you cannot "lock in" a rate for a year.

Financially, you will pay more than if you had opted for a variable rate. However, you are not "losing out" because you have bought peace of mind. You can also (depending on your contract) attempt to renegotiate your mortgage (subrogación, i.e., transferring your mortgage) with another bank to get a better rate, but this incurs fees.

Almost always. To give you the promotional fixed rate (e.g., 3.0%), the bank "incentivises" you in exchange for subscribing to its products: life insurance (seguro de vida), home insurance (seguro de hogar), direct debiting of income (nómina). If you refuse these products, the "normal" (non-incentivised) rate will be much higher (e.g., 4.0%).

Yes, retirees are often considered excellent profiles because they have stable and guaranteed income (their pension). The only limit is age: most banks require the loan to be fully repaid before the age of 75. If you are 65, you will get a loan for a maximum of 10 years.

As a non-resident, you should favour banks that have specialised departments for non-residents, such as Sabadell or Bankinter. Large banks like Santander are excellent, but their local branches are often not well-trained to handle complex non-resident applications. An expert mortgage broker will know which bank to target.

Spanish banks are generally stricter than banks in the UK/US. They apply a rule of 30% to 35% maximum of your net income. They will take into account *all* your liabilities, including rent or loans you have in your home country.

Yes. While it's not 0%, it's a sign of a healthy and stabilised market. Rates around 3% are historically normal and sustainable. The end of 2023-2024 volatility is the best news for buyers, as it brings the necessary visibility to calmly plan a YMYL project like a property purchase.

On the same topic:

Our clients talk about us

Reviews from Peter Z.

"Investor for rent, Murcia"

Satisfied with my investment. Greg top. Duplex flat is good for renting, good return. Service team professional, helps a lot despite my French not perfect. Would recommend.

Reviews from Loïc S.

A delighted investor in Dénia

Reviews from Roxane R.

"Investor in Alicante"

We spoke by phone about a possible future collaboration, and my first impression is very positive. They are serious professionals, full of ideas, which inspires confidence and makes you want to work with them.

Reviews from Inès L.

"Happy buyer, Antequera region"

I'm a delighted buyer in Antequera! Thanks to the agency's professionalism and their invaluable advice, my purchase went off without a hitch. The beauty of the region and the quality of the support provided more than merit my 5/5 rating.

Reviews from Julien G.

"Satisfied buyer, Albarracín region"

As Belgians, we are delighted buyers in the magnificent Albarracín region. Grégory's guidance was exceptional. His in-depth knowledge of the region and its leisure activities, including the golf courses, was a real asset in confirming our choice.

Reviews from Maxence G.

Satisfied buyer, Jávea region

Reviews from Fabien D.

"Retired expatriate in Segovia"

For our retirement project in Segovia, Grégory's guidance was simply perfect. As a keen golfer, he immediately understood our expectations and found us the rare gem just a stone's throw from a magnificent course. Many thanks for his attentiveness and professionalism!

Reviews from Sarah D.

Retired expatriate in Baza

Reviews from Lydia R.

Top!!!

Reviews from Sébastien G.

Owner of a superb flat in Olvera.

Reviews from Mathis R.

Happy owner at Oropesa del Mar

Reviews from Constance B.

Retired expatriate in Baza

Reviews from Gilles B.

Owner of a superb flat in Formentera.

Reviews from Lucie G.

"A delighted investor in La Coruña"

As an investor, I'm absolutely delighted with my project in La Coruña. I was impressed by the quality of the advice and the in-depth knowledge of the local market. The process was extremely smooth and carried out with exemplary professionalism, which is very reassuring for an investment.

Reviews from Jules-Antoine B.

"A delighted investor in Sitges"

As a Belgian investor, I'm delighted with my project in Sitges. The agency's in-depth knowledge of the local market was a major asset in identifying the right investment. The whole process was carried out with great professionalism and efficiency, and I highly recommend it.

Reviews from Quentin P.

Owner of a superb flat in Seville.

Reviews from Édith R.

Owner of a villa in Benalmádena.

Reviews from Christelle W.

"Dentist in Lyon"

Prestigious properties for sale at unbeatable prices in a heavenly setting. French real estate professionals in Spain offering you a fully immersive visit to one of Spain's most beautiful regions. I can't recommend it enough!

Reviews from Emma B.

"Retired expatriate in Vejer de la Frontera"

As a retired expatriate in Vejer de la Frontera, I was delighted with Loreta's support. Her expertise in administrative and legal services gave me invaluable peace of mind. Everything was handled with professionalism and warmth, thank you Loreta!

Reviews from Françoise D.

"Buyer, Guardamar del Segura"

I was very apprehensive at the start of the project, but the young lady was able to reassure me and understood my needs perfectly. The purchase was stress-free.

Reviews from Aurore L.

Happy buyer, Huéscar region

Reviews from Clovis B.

"Satisfied buyer, Carchuna region"

We're delighted buyers at Carchuna! Grégory's support was remarkable. In addition to his great professionalism, his knowledge of local golf courses was a real plus for us. We're delighted to have found the ideal property in which to enjoy our two passions.

Reviews from Jérémy G.

Owner of a villa in Villafranca del Cid.

Reviews from Jean-Pierre L.

"Owner of a villa, Costa Blanca"

Thanks to their help, I found my villa by the sea. Grégory is very friendly and always available.

Reviews from Yohan C.

"Retired expatriate in Grazalema"

Jérôme gave us excellent advice on our retirement project in Grazalema. His expertise in the upmarket market and his mastery of the financial aspects were a real asset in securing our investment. We're delighted to be starting this new life with complete peace of mind.

Reviews from Inès B.

Owner of a superb flat in Orihuela.

Reviews from Valérie V.

"Happy owner in Malaga"

We're finally homeowners in Malaga and we couldn't have hoped for better support. Jérôme's financial expertise and knowledge of the upmarket market enabled us to make our investment with complete peace of mind. Many thanks to him for his professionalism and invaluable advice.

Reviews from Cassandra R.

Owner of a superb flat in Ripoll.

Reviews from Anaëlle N.

Owner of a villa in Archidona.

Reviews from Marie D.

"Happy homeowner in Alicante"

Very happy, an impeccable experience! Grégory was attentive and very professional from start to finish. I would highly recommend him.

Reviews from Ana G.

"Owner of a villa in Castellar de la Frontera."

thank you

Reviews from Lola D.

"Happy owner in Huéscar"

We're finally homeowners in Huéscar and the experience has been perfect. Jérôme's support was essential; his financial expertise enabled us to secure our project with complete confidence and peace of mind. His professionalism and knowledge of the upmarket market are invaluable assets.

Reviews from Sandrine B.

"A delighted investor in Marchena"

As an investor, I am absolutely delighted with my project in Marchena. Grégory's support was exceptional; his knowledge of the region's assets, including the magnificent golf courses, was a real plus for my investment. His professionalism and sound advice are invaluable.

Reviews from Julia P.

"Owner, Santa Pola"

My husband and I are extremely satisfied with the service. We were able to buy our Atico in record time! Many thanks to Jérôme

Reviews from Charlotte C.

"Happy buyer, Cartagena region"

As Belgians, we are delighted buyers in the magnificent Cartagena region. For this first project in Spain, we particularly appreciated the quality of the agency's advice and professionalism. The process was smooth and reassuring from start to finish - a real pleasure!

Reviews from Marie L.

A delighted investor in Barcelona

Reviews from Marion R.

"Owner of a villa in Sayalonga."

We finally own our villa in Sayalonga! A huge thank you to Loreta, whose expertise was invaluable. Her rigorous management of all the administrative and legal aspects enabled us to complete our project with complete peace of mind. It's a real pleasure to have been so well looked after.

Reviews from Myriam M.

"Retired Belgian expatriate, Benidorm"

During my first visit, I had very precise expectations, but I realised that I hadn't communicated my criteria properly. After clarification, Freddy was able to better target my wishes and guide me effectively.

Reviews from Anouk D.

Owner of a superb flat in Torrox.

Reviews from Jérémy B.

Owner of a superb flat in Cadaqués.

Reviews from David G.

Owner of a villa in Santa Pola.

Reviews from Marjorie L.

We have just met Gregory and his agency and what a welcome he gave to our choice of location. We've just started working together and I'd like to thank him warmly. I have no doubt that he will find us our home. Marjorie

Reviews from Isidore F.

Retired expatriate in Estepa

Reviews from Fanny V.

Happy buyer, Albarracín region

Reviews from Bastien G.

Satisfied buyer, Santiago de Compostela region

Reviews from Hélène R.

Retired expatriate in Salamanca

Reviews from Constance G.

Owner of a villa in Benidorm.

Reviews from Zerouki Z.

A serious and responsive team. Thank you for your availability and your personalised advice. I highly recommend you, especially for those looking for a property in Alicante. I wish you all the best!

Reviews from Aurore B.

Owner of a villa in San Fernando.

Reviews from Sébastien D.

"Owner of a villa in Ibiza."

I'm a DJ and it's really a dream come true thanks to Jérome... thank you my Bro