Understanding Senior Mortgage Insurance in Spain: The True Cost & 75-Year Age Limit

Introduction

Buying a property for retirement in the sun is a major life project. Spain, with its climate and quality of life, is a prime destination. However, when it comes to financing this purchase, 'senior' buyers (generally 55 and over) face a complex financial reality. The question isn't just whether one can borrow, but at what cost, and crucially, for how long.

As experts in property financing for non-residents in Spain, we must clarify two misconceptions. Firstly, the mortgage insurance rate (seguro de vida) is not the sole obstacle; it does increase with age, but the true challenge lies elsewhere. The real impediment is the repayment age limit, set by most Spanish banks at 75 years old. This article analyzes the actual cost and constraints of senior borrowing in Spain.

The Real Hurdle: The 75-Year Age Limit Rule

This is the golden rule that overrides all others: most Spanish banks (Sabadell, CaixaBank, BBVA...) require the borrower to have fully repaid their mortgage before their 75th birthday. A few rare institutions may extend this to 80 years, but 75 is the market standard.

This rule has a direct and mechanical consequence: it drastically reduces your loan term. The later you borrow, the shorter the repayment period. A shorter term means higher monthly repayments, which must still adhere to the maximum debt-to-income ratio of 30-35% of your income.

The Impact of Age on Loan Duration: The 'Scissor Effect'

For a property purchase, a short loan term is often a greater impediment than the interest rate itself. Here's the 'scissor effect' of the 75-year rule on your maximum loan duration (plazo de amortización).

| Your Current Age | Maximum Loan Duration | Consequence |

|---|---|---|

| 60 years old | 15 years | Manageable monthly repayments. |

| 65 years old | 10 years | High monthly repayments, reduced borrowing capacity. |

| 68 years old | 7 years | Very high monthly repayments, loan often refused (debt-to-income ratio exceeded). |

| 70 years old and above | 5 years or less | Classic mortgage approval almost impossible. |

The True Cost: Rates and Calculation of Senior Insurance (Seguro de Vida)

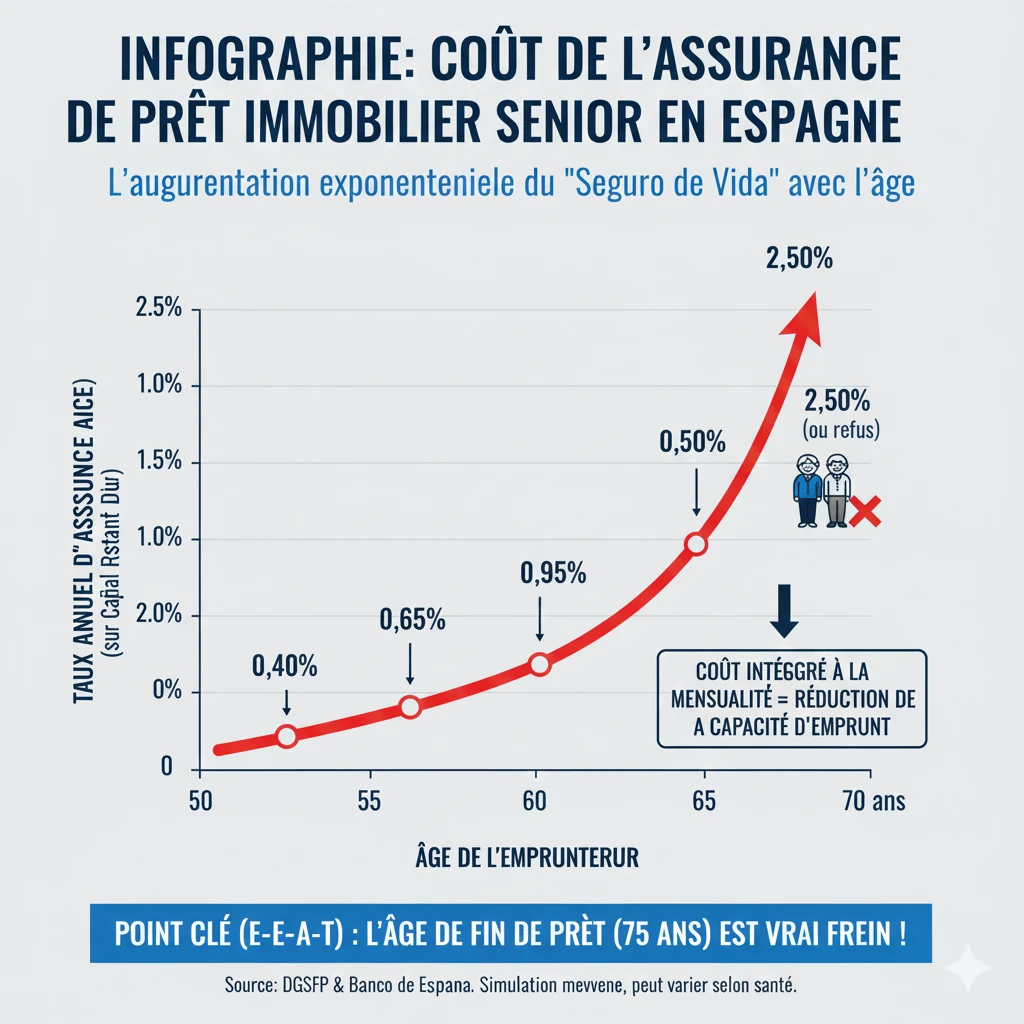

The second obstacle is the cost of life and disability insurance (Seguro de Vida). While not legally mandatory (unlike home insurance), it is required by the bank to secure the loan. Its cost is calculated based on your age, health status, and the capital borrowed.

For seniors, this cost is not negligible and increases exponentially. It is directly integrated into your monthly repayment (APR) and thus impacts your debt-to-income ratio.

The Trap of the "Prima Única Financiada" (Single Premium)

Many Spanish banks offer seniors the option to pay for insurance in a single installment via a "Prima Única" (Single Premium). They propose including it in the borrowed capital. This is a very disadvantageous solution:

- Increased Capital: If you borrow €100,000 and the insurance costs €15,000, the bank provides a loan of €115,000.

- Interest on Insurance: You pay interest (at the loan rate) on the cost of your insurance for the entire loan term!

Our expert advice: Always insist on an annual premium (Prima Anual) payment, even if the bank pushes its 'in-house' single premium insurance.

| Age Range | Estimated Average Annual Rate |

|---|---|

| 50-55 years old | 0.40% - 0.60% |

| 56-60 years old | 0.65% - 0.90% |

| 61-65 years old | 0.95% - 1.40% |

| 66-70 years old | 1.50% - 2.50% (or refusal) |

Solutions for Borrowing in Retirement

Faced with the dual constraints of age (75 years) and insurance costs, solutions for retirees focus on reducing risk for the bank.

- Increase Your Personal Down Payment (Acompte)

This is the simplest solution. As a non-resident, the minimum down payment is 30% (+12% fees). As a senior, a 50% or 60% down payment significantly reduces the capital borrowed. A smaller capital over a short term (10 years) can result in monthly repayments that respect your debt-to-income ratio. - The Co-Borrower (Cotitular)

This is the most effective solution. If you borrow with a younger child (or a third party), the bank will calculate the loan term based on the age of the youngest co-borrower. If your daughter is 40, you could potentially borrow over 20 or 25 years, which significantly lowers the monthly repayment. - Pledging Assets (Pignoración)

If insurance is refused or prohibitively expensive, you can offer to pledge (block) a sum of money (e.g., from a life insurance policy or investment account) as collateral. Should you pass away, the bank can draw from this blocked capital.

The Case of the "Hipoteca Inversa" (Reverse Mortgage)

Be aware that the "Hipoteca Inversa" is not a loan to purchase a property. It is a product intended for seniors (generally 65+) who already own their home in Spain (without an existing mortgage) and wish to receive a monthly income by mortgaging their own property.

Official Resource

Regulations for mortgage-related insurance in Spain are overseen by the DGSFP (Dirección General de Seguros y Fondos de Pensiones - General Directorate of Insurance and Pension Funds) and the Bank of Spain. You can consult your consumer rights on their portal.

Conclusion

Borrowing in Spain during retirement is a challenge, but it is not insurmountable if the project is well-structured. The real obstacle is not so much the mortgage insurance rate, although it is high, but the 75-year age limit imposed by banks.

This constraint mechanically shortens your loan term, pushing monthly repayments beyond the permissible debt-to-income threshold. Our expertise (Experience) shows that the only two viable solutions for a senior purchase are to reduce the borrowed capital through a substantial down payment (over 50%) or to add a younger co-borrower to extend the loan term.

Is Your Senior Financing Project Viable?

Take advantage of market opportunities. Let's discuss your project.

Article Summary

FAQ : Mortgages for Retirees in Spain (Senior Loans)

Our experts address the challenges of age limits (75 years) and insurance costs.

The true hurdle isn't the cost of insurance, but the maximum age for mortgage repayment. Most Spanish banks require the mortgage to be fully settled before your 75th birthday.

This is the golden rule for senior mortgage applicants in Spain. Banks (Sabadell, CaixaBank, BBVA...) calculate your mortgage term to ensure your final monthly repayment is made before you reach the age of 75. A few rare lenders might extend to 80 years, but 75 is the standard.

The maximum term for your mortgage will be 10 years (75 years - 65 years = 10 years). If you are 68, the maximum term drops to 7 years.

Because a short repayment term automatically results in a higher monthly repayment. This elevated monthly payment is likely to exceed the maximum debt-to-income ratio permitted by the bank (typically 30-35% of your income), leading to a mortgage application refusal.

It is almost impossible. At 70, the maximum term would be 5 years, generating such high monthly repayments that the debt-to-income ratio is almost always exceeded.

It's the second obstacle, but not the primary one. Its cost is high and impacts the debt-to-income ratio, but the main barrier remains the mortgage term imposed by the 75-year rule.

The cost increases exponentially with age. It is estimated that between 61 and 65 years old, the average annual rate is between 0.95% and 1.40% of the outstanding capital. Between 66 and 70 years old, it can climb from 1.50% to 2.50% per year, or even result in an insurance refusal.

No, it is not legally mandatory (unlike building insurance). However, it is practically required by the bank to secure the mortgage in case of death or disability.

This is a 'pitfall' offered by many Spanish banks. They propose you pay the insurance in a single lump sum (Single Premium) and to include this amount in the principal of your mortgage.

It's a very poor solution because you end up paying interest on the cost of your insurance. If you take out a mortgage for €100,000 and the insurance costs €15,000, the bank lends you €115,000, and you pay interest on the total amount.

You should insist on paying an annual premium (Prima Anual). You pay the insurance annually, its cost is calculated on the outstanding balance (and therefore decreases over time), and you do not pay interest on the insurance cost itself.

This article identifies three main solutions:

-

Increase your down payment (Acompte): Aim for a 50% or 60% down payment to reduce the capital borrowed.

-

Add a co-borrower (Cotitular): Apply for the mortgage with a younger person (e.g., a child).

-

Pledging assets (Pignoración): Secure a sum of money (e.g., a life insurance policy) as collateral if mortgage life insurance is refused.

The most effective solution is to add a younger co-borrower. The bank will calculate the maximum mortgage term based on the age of the youngest co-borrower, allowing you to secure a mortgage for 20 or 25 years and drastically reduce the monthly repayments.

While a typical non-resident international buyer usually needs to provide a 30% down payment (+ additional fees), a senior buyer is advised to aim for a 50% or 60% down payment. This significantly reduces the mortgage amount, making it more likely that the monthly repayments (even over a 10-year term) will fall within the permitted 35% debt-to-income ratio.

No. The article clearly states: the 'Hipoteca Inversa' is not a loan designed for purchasing a property. It is a financial product intended for seniors who are already homeowners in Spain and wish to receive an income or regular payments by leveraging the equity in their existing home.